Fixed Asset Management Fundamentals

What are Fixed Assets? Fixed assets are long-term resources owned by a company that are used in its operations and provide economic benefits over multiple accounting periods. They come in various forms – tangible assets (physical items like land, buildings, machinery, vehicles, equipment), intangible assets (non-physical assets like software, patents, goodwill), and sometimes financial assets (long-term investments, securities)[1][1]. These assets are capitalized on the balance sheet rather than expensed immediately, because they have a useful life spanning multiple years. For example, a $300 printer expected to last 3 years would be recorded as an asset and expensed $100 per year over its life, rather than $300 all in the first year[1]. Most accounting standards (e.g. IFRS and GAAP) mandate such treatment to match the asset’s cost with the revenue it helps generate over time (the matching principle).

Role in Financial Accounting: Fixed assets (often called Property, Plant, and Equipment or PPE under IAS 16) are critical to a company’s operations and financial position. They represent significant investments and are subject to special accounting rules for capitalization (recording on the balance sheet), depreciation (systematically expensing their cost), and impairment or disposal. Proper fixed asset accounting ensures that a company’s financial statements reflect the current value and remaining useful life of these assets, and that expenses are recognized in the correct periods. Fixed assets are usually reported at cost minus accumulated depreciation (under the cost model) or at revalued amounts (under the revaluation model, if adopted)[2][2]. Intangible assets are accounted for in a similar way (amortized if they have finite life, or tested for impairment if indefinite life). Financial assets follow separate standards (e.g. IFRS 9) and are not depreciated, but are worth noting as non-current assets that may be carried at fair value or amortized cost depending on their nature.

Asset Lifecycle Stages: Every fixed asset goes through a lifecycle with several key stages[3]:

- Acquisition/Capitalization: The asset is purchased or otherwise acquired and recognized on the balance sheet. All costs necessary to bring the asset to working condition for its intended use are capitalized (purchase price, import duties, installation, initial delivery, site preparation, etc.)[2][2]. For example, if equipment is bought outright, the journal entry would debit the asset account and credit Cash or Payables for the total cost (including any shipping or installation)[3][3]. If acquired via exchange or non-monetary transaction, IFRS prescribes using fair value if available[2]. The date the asset is available for use often marks the start of depreciation.

- Depreciation (or Amortization for intangibles): Over the asset’s useful life – the period it is expected to generate benefits – the company systematically allocates the asset’s depreciable cost to expense. Depreciation is “the systematic allocation of the depreciable amount of an asset over its useful life”[2]. This matching of cost to periods of benefit adheres to accrual accounting[2]. Depreciation methods and rates are chosen based on the asset’s usage pattern and reviewed annually[2][2] (we delve into methods in the next section). Each period’s depreciation is recorded as an expense on the income statement and accumulated as Accumulated Depreciation on the balance sheet (a contra-asset reducing the asset’s carrying amount). The typical journal entry is a debit to Depreciation Expense and a credit to Accumulated Depreciation[3][3]. Depreciation continues until the asset is fully depreciated or removed from service.

- Maintenance and Use: Throughout its life, the asset may incur maintenance, repairs, or improvements. Ordinary repairs are expensed, but significant improvements or upgrades that extend the asset’s life or capacity are capitalized (added to the asset’s cost per IAS 16). The asset may also be transferred between locations or departments. Enterprise systems allow tracking asset movements (e.g., change of location or custodian) and linking maintenance schedules to the asset record[4]. Proper maintenance management ensures assets reach their expected life.

- Revaluation (IFRS option) or Value Adjustment: Under certain standards (like IFRS), companies can choose the revaluation model for classes of assets – meaning they periodically adjust an asset’s carrying amount to fair value and recognize changes in equity (revaluation surplus) or profit/loss (subject to IFRS rules)[2][2]. Revaluation increases are generally recorded in OCI (equity) as a revaluation surplus, except to the extent they reverse a previous revaluation decrease that was expensed; decreases are expensed to profit/loss, except if reversing a prior surplus[2]. Revaluation ensures the balance sheet reflects current values, but it requires regular fair value assessments. Outside of formal revaluation, other value adjustments include impairment write-downs if an asset’s recoverable amount falls below its carrying amount (see below), or adjustments for changes in useful life or residual value (treated prospectively as changes in estimate).

- Impairment: If an asset becomes significantly devalued due to damage, obsolescence, or market changes, an impairment test is conducted (per IAS 36). An impairment loss is recognized if the asset’s carrying amount exceeds its recoverable amount. The loss is recorded in profit or loss, reducing the asset’s carrying value. For instance, if a piece of machinery is damaged and can no longer generate expected future cash flows, it may be written down (Dr. Impairment Loss, Cr. Asset or Accumulated Impairment). IFRS requires annual impairment assessment for certain assets and when indicators of impairment exist[2]. Any compensation from third parties (e.g., insurance for damaged assets) is recognized in income when receivable[2].

- Disposal/Retirement: Eventually, the asset is derecognized – either through sale, scrapping, or retirement. Derecognition occurs when the asset is disposed of or no future economic benefits are expected from its use[2]. At disposal, the asset’s cost and accumulated depreciation are removed from the books, and any proceeds from sale are recorded. A gain or loss is computed as the difference between net proceeds (if any) and the asset’s book value (cost minus accum. depreciation)[3]. For example, selling a fully depreciated machine for $5,000 would be recorded as: debit Cash $5,000, debit Accumulated Depreciation (to remove it), credit the Asset’s cost, and credit Gain on Disposal for the difference (if proceeds exceed book value)[3][3]. If disposed for no proceeds (scrapped), any remaining book value is a loss. Enterprise asset modules often have functions for asset retirement or scrapping that automatically post these entries and record the reason for disposal. Proper disposal accounting ensures no “ghost assets” remain on the books after they’re gone[5].

This lifecycle approach – from acquisition to depreciation to revaluation/impairment to disposal – keeps financial records accurate and compliant. Each stage corresponds to specific journal entries and processes[3][3]. Modern ERP systems maintain a detailed asset register so that all these events (purchase, transfers, depreciation, revaluation, maintenance, disposal) are tracked against each asset record[1]. This provides an audit trail and ensures that an asset’s history and current status (e.g. location, condition, remaining life, book value) are transparently recorded. Many systems also support asset maintenance logs and asset movements (for tracking physical location changes) and component accounting (depreciating significant parts of an asset separately, per IFRS componentization guidance)[2].

Relevant Accounting Standards: Fixed asset accounting is governed by standards to ensure consistency:

- IFRS/IAS: The primary standard is IAS 16 “Property, Plant and Equipment”, which covers recognition, measurement (cost vs revaluation model), depreciation, and derecognition of tangible assets[2][2]. IAS 38 covers intangibles (similar principles, though intangibles can’t be revalued to create a revaluation surplus except if an active market exists). IAS 36 covers asset impairments, and IAS 23 covers capitalization of borrowing costs on qualifying assets. For foreign currency aspects, IAS 21 “The Effects of Changes in Foreign Exchange Rates” provides rules on how to record assets acquired in foreign currencies and translate financial statements (more on this in the multi-currency section). IAS 16 requires regular review of useful lives, residual values, and depreciation methods, and allows the cost model (assets carried at cost minus depreciation) or revaluation model (assets carried at fair value minus depreciation)[2]. It also stipulates that depreciation begins when the asset is available for use and continues until derecognition (even if idle, unless fully depreciated or classified as held-for-sale)[2]. Another IFRS to note: IAS 10 (events after reporting) for situations like assets destroyed after year-end, IFRS 5 if an asset is held for sale, etc., and IAS 24 for any related-party asset transfers.

- US GAAP: While this study focuses on IFRS, US GAAP has similar concepts under ASC 360 (PPE) and others, with the main difference being that revaluation is not permitted under GAAP (assets stay at cost minus depreciation). GAAP and IFRS both require depreciation expense on the income statement and similar impairment tests (though details differ). For tax purposes, many jurisdictions prescribe specific depreciation systems (e.g., MACRS in the US) which often differ from book depreciation, necessitating separate tracking (e.g., via separate depreciation books or schedules).

- Local Regulations: Many countries (including Arab Gulf countries) have adopted IFRS for financial reporting. For example, Gulf Cooperation Council (GCC) countries like Saudi Arabia, UAE, Oman, etc., largely require IFRS for listed and large enterprises. In Saudi Arabia, “SOCPA GAAP” was aligned with IFRS and now IFRS is mandatory for listed companies. Smaller companies might follow simplified local standards, but the fundamental principles (capitalizing long-lived assets and depreciating them) remain. Additionally, tax laws often define depreciation rates or methods for tax deduction purposes, which may require maintaining parallel records (one for book/IFRS and one for tax).

In summary, fixed assets are critical resources that must be capitalized and then expensed over time via depreciation. A clear understanding of their lifecycle and relevant accounting standards ensures that both small businesses and large enterprises properly manage these assets on their books, maintain compliance (for example, with IAS 16 for recognition and depreciation and IAS 21 for any currency issues), and extract full value from their assets through effective tracking and maintenance.

Depreciation Concepts and Methods

Purpose of Depreciation: Depreciation is the accounting process of allocating an asset’s cost to expense over the periods that benefit from its use. It reflects the wear-and-tear, usage, or obsolescence of the asset. Rather than taking a huge expense when an asset is purchased, we spread the cost systematically across its useful life[2]. This upholds the matching principle: as the asset helps generate revenue over multiple years, a portion of its cost is expensed each year to match against those revenues[2]. Depreciation does not involve cash outflow in the period; it’s a non-cash expense that gradually writes down the asset’s book value and accumulates on the balance sheet as Accumulated Depreciation. By the end of the asset’s life, the total depreciation taken equals the depreciable amount (cost minus any estimated salvage value), and the asset’s net book value equals the salvage value (or zero if none).

Impact on Financial Statements: Depreciation expense appears on the Income Statement, reducing reported profit. On the Balance Sheet, it reduces the asset’s carrying amount via accumulated depreciation (a contra-asset). Over time, as depreciation accumulates, the net book value of the asset declines, indicating how much of the asset’s economic value has been “used up.” Importantly, depreciation affects taxes: in many tax regimes, depreciation on long-term assets is deductible, thus reducing taxable income (subject to specific tax rules). Accelerated depreciation methods can defer tax payments by yielding higher expense (lower taxable income) in early years[6][6]. However, for financial reporting under IFRS/GAAP, companies choose methods that best reflect the asset’s usage pattern, and these choices impact the timing of expense recognition and profits. It’s common to maintain separate “book depreciation” (for financials) and “tax depreciation” (for tax filings) if methods or rates differ, with differences giving rise to deferred tax adjustments.

From an investor’s perspective, depreciation reduces net income (a negative impact on short-term profit) but is added back in cash flow statements (since it’s non-cash). Over an asset’s life, total expense will equal cost regardless of method, but the timing differs. Accelerated depreciation leads to lower accounting profits in early years and higher in later years (and vice versa for slow methods), which can affect financial ratios and performance indicators. Choosing a method is often about faithful representation of asset use rather than earnings management – for example, if an asset truly loses value faster initially (like tech gadgets), an accelerated method better reflects economic reality[6][6].

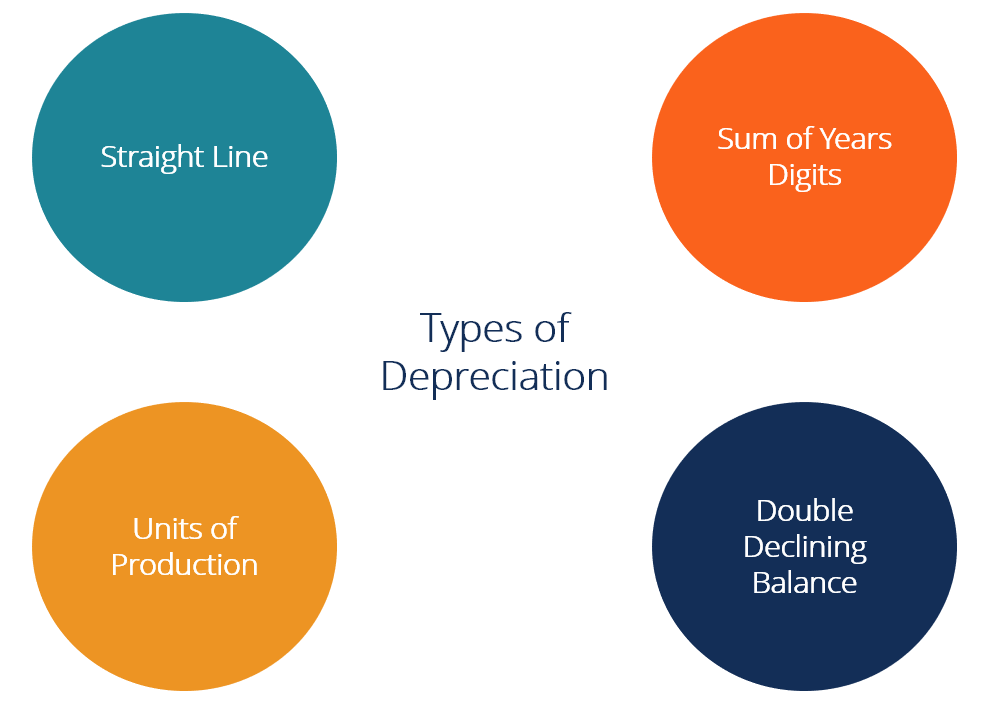

Common Depreciation Methods: Different assets and contexts call for different depreciation techniques. The main methods include[7][7]:

- Straight-Line Depreciation: This is the simplest and most widely used method. It expenses an equal amount each period over the asset’s useful life. Formula:

- Depreciation Expense (per period)=Cost – Salvage ValueUseful Life\text{Depreciation Expense (per period)} = \frac{\text{Cost – Salvage Value}}{\text{Useful Life}}Depreciation Expense (per period)=Useful LifeCost – Salvage ValueIt assumes the asset’s utility (or the economic benefit) is consumed evenly over time[7][7]. For example, a $25,000 asset with zero salvage and 8-year life depreciates $3,125 per year (which is $25,000/8)[7][7]. Straight-line is often appropriate for assets that wear out evenly (e.g., furniture, buildings) and has the advantage of simplicity and stable expense recognition each period.

- Declining Balance (Accelerated) Depreciation: This method allocates higher depreciation in the early years and less in later years. The rationale is that many assets (like technology or vehicles) are more productive or lose value faster when new[7]. A common variant is Double-Declining Balance (DDB), which is a declining balance method with a factor of 2× the straight-line rate. Formula for DDB:

- Depreciation Expense=Beginning Book Value×2Useful Life\text{Depreciation Expense} = \text{Beginning Book Value} \times \frac{2}{\text{Useful Life}}Depreciation Expense=Beginning Book Value×Useful Life2In practice, one computes a constant rate = 2×(1/Life) and applies it to the asset’s beginning net book value each year[7][7]. Because book value decreases each year (cost minus accum. depreciation), the dollar depreciation shrinks over time. For example, if $25,000 asset, 8-year life, salvage $2,500: straight-line rate =12.5%, double rate =25%. Year 1 depreciation = 25% of $25k = $6,250; book value becomes $18,750. Year 2: 25% of $18,750 = $4,687.5, and so on[7][7]. One caveat: DDB does not automatically stop at salvage value, so typically in the final year or two, companies switch to straight-line or otherwise ensure the asset isn’t over-depreciated. The accelerated methods front-load expenses, which reduces taxable income in early years (a tax benefit)[6] and can better reflect actual usage patterns for certain assets[6][6]. The downside is lower profits initially (and higher later), and more complexity. Another variant is 1.5 declining balance (150% of straight-line rate), or generally diminishing balance with any factor.

- Sum-of-the-Years’ Digits (SYD): Another accelerated method, SYD also yields higher depreciation in early years and lower in later years, but in a slightly different pattern. It uses a fraction based on remaining life over the sum of all years’ digits. Formula:

- Depreciation Expense=Remaining Life in YearsSum of all Years×(Cost – Salvage).\text{Depreciation Expense} = \frac{\text{Remaining Life in Years}}{\text{Sum of all Years}} \times (\text{Cost – Salvage}).Depreciation Expense=Sum of all YearsRemaining Life in Years×(Cost – Salvage).The “sum of years” for an $n$-year life is n+(n-1)+...+1 = n(n+1)/2. For instance, if life = 5 years, sum = 15. The first year depreciation would use fraction 5/15 of depreciable amount, second year 4/15, etc. This yields a sequence of depreciation charges that decrease each year. The SYD formula is explicitly[7]. In a 3-year, $53,000 depreciable base example, SYD would allocate $26,500 in Year1, $17,667 in Year2, $8,833 in Year3 (given sum=6, remaining life fractions 3/6, 2/6, 1/6)[3][3]. SYD is slightly less aggressive than double-declining in early years, but more than straight-line. It’s conceptually similar to declining balance in aiming to reflect usage/value drop earlier.

- Units-of-Production (or Usage-Based) Depreciation: This method ties depreciation to actual usage of the asset rather than time. A total output or usage capacity is estimated (e.g., machine hours, units produced, miles driven), and depreciation per unit is calculated. Formula:

- Depreciation Expense=Units Produced this periodTotal Units over Life×(Cost – Salvage).\text{Depreciation Expense} = \frac{\text{Units Produced this period}}{\text{Total Units over Life}} \times (\text{Cost – Salvage}).Depreciation Expense=Total Units over LifeUnits Produced this period×(Cost – Salvage).In effect, a rate per unit is determined: (Cost–Salvage) / Total expected units[7]. Each period, that rate is multiplied by actual units that period. This method matches expense with actual wear-and-tear. For example, a delivery truck costing $50,000 with expected 100,000 miles and $5,000 salvage: depreciable $45,000; rate = $0.45 per mile. If it’s driven 20,000 miles in Year1, depreciation = 20,000 × $0.45 = $9,000 Year1. If only 5,000 miles in Year2, depreciation = $2,250, and so on. Units-of-production is ideal for assets whose utility is best measured in usage terms (factory machines, vehicles, etc.), so heavy use periods incur more expense. It results in variable expense each period, reflecting activity levels.

Choosing a Method: The appropriate method depends on the asset’s consumption pattern of economic benefits. IFRS states the method should reflect the expected pattern of asset use[2][2]. If benefits are evenly consumed, straight-line is fine. If an asset’s value or productivity declines faster initially (e.g., high-tech equipment becoming obsolete quickly or a new car losing value when driven off the lot), an accelerated method is warranted[6][6]. Units-of-production is suitable when wear is directly linked to output or usage (like depreciating an aircraft engine by flight hours). The method is not set in stone: if expectations change (say, usage pattern changes or company realizes a different pattern of benefits), IFRS and GAAP allow changing the depreciation method prospectively as a change in estimate (with disclosure)[2][2].

Depreciation Formula Recap:

- Straight-line: Expense = (Cost – Salvage) / Life[7].

- Declining Balance: Expense = Opening book value × (Accelerated Rate). For DDB, Rate = 2 × (1/Life)[7].

- Sum-of-years-digits: Expense = (Remaining life / sum of years) × (Cost – Salvage)[7].

- Units-of-production: Expense = (This period’s units / total life units) × (Cost – Salvage)[7].

Types of Depreciation Methods. Different methods allocate an asset’s cost in varying patterns (evenly with straight-line, front-loaded with accelerated methods, or based on usage). Each method has its rationale and financial impact, affecting profit timing and tax. Companies often use straight-line for its simplicity and consistency, but will use accelerated or usage-based methods when appropriate to reflect how an asset’s value is consumed[6][7].

Journal Entry Examples: Regardless of method, the periodic entry to record depreciation is generally:

- Debit Depreciation Expense (P&L)

- Credit Accumulated Depreciation (B/S contra-asset).

For instance, if monthly depreciation on a machine is $1,000, each month: Dr Depreciation Expense $1,000; Cr Accumulated Depreciation $1,000[3][3]. Over time, Accumulated Depreciation grows, reducing the asset’s carrying amount.

If an asset is disposed, the depreciation for the final period is taken up to the disposal date. Then a disposal entry is made: remove asset cost (credit asset), remove accumulated depreciation (debit it), record any proceeds (debit cash or receivable), and the difference goes to Gain or Loss on Disposal[3][3]. Example: equipment cost $100k, accum. depreciation $80k, sold for $54k cash. Entry: Dr Cash $54k, Dr Accum. Depr $80k, Cr Equipment $100k, Cr Gain on Disposal $34k (because $54k proceeds – $20k NBV = $34k gain)[3][3]. Conversely, if proceeds were less than NBV, the difference is a loss (debit). These entries ensure the asset and related depreciation are fully removed and any gain/loss is recognized in income[3][3].

Depreciation and Tax Reporting: As noted, depreciation can significantly impact taxes. Tax authorities often prescribe specific methods or rates (often accelerated to encourage capital investment). The difference between book depreciation (for financial reports) and tax depreciation (for IRS/tax authority) can lead to deferred tax effects. For example, if tax depreciation is faster, early years see lower taxable income (tax savings) but the company might report higher book income (due to slower book depreciation). Over the asset life, total depreciation converges, but timing differences create deferred tax liabilities or assets on the balance sheet. Companies maintain reconciliation of book vs tax depreciation. In some ERPs (like NetSuite, SAP), this is handled by multiple depreciation books: one for corporate (book/IFRS) and one for tax, allowing parallel calculation.

From a compliance perspective, companies must disclose their depreciation methods, useful lives or rates, and total depreciation expensed in notes to the financial statements. Auditors check that useful lives are reasonable and that any changes in estimate are properly accounted for (prospectively) and disclosed. They also verify that no assets are over-depreciated or still carried when fully depreciated and not in use.

Key Takeaway: Depreciation is an essential concept that impacts both the profitability and asset values in financial reports. It offers a means to save on taxes (by deducting asset costs over time) but must be grounded in the asset’s actual usage and benefit pattern. Accelerated depreciation can reduce taxable income in early years[6], while straight-line offers simplicity and steady expense. Choosing the right method and correctly computing depreciation ensures fair presentation of financials and compliance with accounting standards. As one source notes, selecting a depreciation method can “significantly impact a business’s financial statements and tax obligations,” and should align with the nature of the asset and the company’s financial strategy[6].

Multi-Currency Asset Accounting

In today’s global economy, many companies purchase assets in foreign currencies or operate assets in multiple countries. Multi-currency asset accounting deals with how to record and report fixed assets when more than one currency is involved – whether it’s an asset purchased in a foreign currency, or assets held by subsidiaries whose functional currency differs from the group’s reporting currency. Two major considerations are: (1) accounting for foreign currency transactions (e.g., buying a machine in EUR for a company whose books are in USD), and (2) translating asset values for consolidated financial reporting if the company has foreign operations. The rules are defined by standards like IAS 21 in IFRS, and similar guidelines in other GAAPs, to ensure consistency in handling exchange rate effects.

Initial Recognition of Foreign Currency Assets: When a fixed asset is acquired in a foreign currency, the transaction is initially recorded in the entity’s functional currency using the spot exchange rate on the date of transaction[8][8] (IAS 21.21). For example, if a European subsidiary of a US company buys equipment for €100,000 and its functional currency is EUR, it records it at €100,000. But if a US-based company (USD functional currency) buys equipment priced in EUR, and the exchange rate on purchase date is €1 = $1.10, it records the asset at $110,000 on that date (and a corresponding liability if on credit). IAS 21 also allows a practical expedient of using an average rate for the period if rates don’t fluctuate significantly[8], but for a large one-time asset purchase, usually the spot rate on the transaction date is used for precision.

After initial recognition, how do exchange rate changes affect the asset’s book value? The crucial point: a fixed asset is a non-monetary item (its value is not a fixed number of currency units; it’s tied to its historical cost or fair value)[8]. According to IAS 21, non-monetary items carried at historical cost are not retranslated at each balance sheet date for exchange rate changes[8]. They remain at the original rate (historical cost in functional currency). This means once the USD functional company recorded that machine at $110,000, it will keep reporting it at $110,000 (minus depreciation) going forward, regardless of EUR/USD moves – unless some other event (like impairment or revaluation) triggers a remeasurement. Any monetary liabilities related (like an accounts payable for the machine if not yet paid) are revalued each period, giving rise to exchange gains/losses that go to P&L[8][8]. But the asset’s carrying value itself doesn’t change with forex rates if using historical cost.

Example: A US company’s functional currency is USD. It buys a machine for €100,000 on Jan 1 when EUR/USD = 1.1 ($110k). It records: Dr Asset $110k; Cr Accounts Payable $110k. By Feb 1, when it pays the supplier, assume EUR/USD moved to 1.2 (now €100k = $120k). The company will pay $120k to settle the payable. At payment, the Accounts Payable (monetary liability) is updated from $110k to $120k, and the $10k difference is an FX loss in P&L. The Asset remains at $110k on books (non-monetary, not updated for FX)[8][8]. The end result: the asset stays at the USD cost equivalent at purchase date, the extra $10k paid is recorded as a loss. If the rate had gone the other way (say 1.0, requiring only $100k to pay off $110k recorded payable), the $10k would be an FX gain. The asset’s value is insulated from currency fluctuations after initial recognition (unless you choose to revalue the asset entirely, see revaluation model later). As IFRScommunity succinctly states: “the PP&E item is carried at historical cost and is not subsequently retranslated to reflect exchange rate movements…”[8].

Non-Monetary Items at Fair Value: If a non-monetary asset is carried at fair value (for instance, if the company uses the revaluation model under IAS 16, or for investment property at fair value, etc.), and that fair value is determined in a foreign currency, then you translate that fair value using the rate at the date of measurement[8]. For example, suppose a UK company (GBP functional) owns land in the US, carried at fair value. If it revalues the land at $1 million on Dec 31 and GBP/USD is 0.75, it would record it at £750k. If next year rate changes and another valuation in USD is done, that new fair value would be converted at that time’s rate. Importantly, exchange differences in such cases aren’t separately recorded as FX gain/loss; they’re folded into the revaluation change. IAS 21 clarifies that for non-monetary assets measured at fair value, the treatment of any exchange difference is governed by the standard driving the measurement[8][8] – e.g., a revaluation surplus from a foreign PPE revaluation goes to OCI, and any FX effect is inherently in that OCI change.

Depreciation in Functional Currency: Once recorded, depreciation of the asset is computed in the functional currency on the functional-currency carrying amount. In the example, the $110k machine depreciates, say over 10 years, $11k/year in the US books. The company does not re-compute depreciation each month based on new exchange rates – it sticks with the functional currency amount. Thus, the income statement is not volatile to currency swings for that asset (aside from the one-time FX impact on purchase if payment timing differed). This stability is because fixed assets are treated as non-monetary. Contrast this with a monetary asset (like a foreign currency loan receivable) which would get revalued at each period-end, causing recurring FX gains/losses.

Consolidation and Presentation Currency: If the company has foreign subsidiaries, those subs will have their own functional currencies. When consolidating into a group (presentation) currency, assets on the subs’ balance sheets need to be translated. Under IFRS consolidation rules (IAS 21 for translating foreign operations), assets and liabilities of a foreign subsidiary are translated at the closing rate (end-of-period exchange rate) into the group’s presentation currency[8][8]. For example, a Saudi subsidiary (functional currency SAR) that holds a piece of equipment at SAR 100,000 net book value will translate to USD at the closing USD/SAR rate for the consolidated statements of the US parent. This translation adjustment does not affect the subsidiary’s local books, but it does create differences in the consolidated equity. Exchange differences arising from translating a foreign operation’s net assets to the parent currency are recorded in a special equity account, often called Cumulative Translation Adjustment (CTA) or Foreign Currency Translation Reserve (FCTR)[8][8]. These differences go to OCI (bypassing P&L) and accumulate in equity until disposal of the foreign operation[8][8]. This way, fluctuations in foreign asset values due to currency are reflected in equity and don’t distort the income statement. For instance, if a UK subsidiary’s £-denominated fixed assets gain value in USD terms because the pound strengthened, the increase is a positive CTA in consolidated equity.

To summarize that: within an entity’s own books – a fixed asset’s value is frozen at the historical exchange rate (if cost model)[8]. For group reporting – foreign entities’ asset values will move with exchange rates at consolidation, but those movements are kept in OCI (CTA)[8][8]. This aligns with IFRS and US GAAP practices ensuring that currency translation gains/losses from long-term assets don’t hit operational profit.

Functional Currency vs Transaction Currency: It’s important to differentiate the functional currency (the primary currency of the company’s environment) from a transaction (foreign) currency. IAS 21 requires that transactions in foreign currencies are initially recorded in the functional currency, as discussed, and any monetary items (like payables, receivables) are revalued at closing rates until settled[8][8]. The functional currency is determined by factors like the currency that influences sales prices, costs, and financing of the entity[8] – essentially the currency of the primary economic environment. Once set, the functional currency dictates how results are measured; foreign currency transactions are secondary. For fixed assets, typically a company’s functional currency is used for its asset ledger.

Multi-Currency Accounting in Practice: Modern ERPs allow companies to designate currencies for transactions and maintain base currency reporting. For example, in ERPNext or NetSuite, you can input a purchase invoice in a foreign currency; the system will either use a stored exchange rate or prompt for one to record the asset value in the company’s base (functional) currency[9][9]. Systems often have a currency exchange rate table that can fetch rates (some even integrate with FX rate feeds)[9]. Controls exist: e.g., ERPNext requires checking a “Multi Currency” option on journal entries that involve accounts of different currencies as a safety mechanism[10][10] – as seen when an asset in USD for a JOD-base company required enabling multi-currency for depreciation posting. This is to ensure proper handling and user awareness when debiting/crediting accounts in differing currencies.

Foreign Exchange Gains/Losses: As noted, when buying an asset on credit in foreign currency, the payable is monetary. Any difference between initial recording of the payable and actual payment goes to FX gain or loss in the income statement[8][8]. However, the asset’s recorded cost remains at the original rate. Thus, the overall cost in functional currency may end up slightly higher or lower than initially recorded once payment is done, with the difference absorbed as FX gain/loss. IFRS prohibits retroactively adjusting the asset’s cost for such exchange differences (except in rare circumstances such as hyperinflation or if using certain allowed alternative treatments for very specific cases). The logic is, once the asset is on books, it’s a non-monetary item.

One special scenario: if an entity uses the revaluation model and the asset is revalued in a foreign currency, the increase/decrease is handled per IAS 16 through revaluation surplus or P&L, as discussed, and any currency effect is inherently in that revaluation. Another scenario: impairment of a foreign-currency asset – since recoverable amount might be estimated in foreign currency, you’d compute that and then translate at the rate on the impairment test date, compare to carrying (which is at historical rate), any impairment loss is recognized in functional currency P&L.

Multi-Currency Presentation in Financials: Companies must disclose how they handle foreign currency items. IFRS requires disclosure of exchange differences recognized in profit or loss and in OCI, and the closing rates used, etc. On financial statements, typically fixed assets on the balance sheet are in the reporting currency. If notes present a fixed asset register, they might show the original currency cost and exchange rate used if relevant, especially for consolidated statements. In the Arab Gulf, currencies like Saudi Riyal or UAE Dirham are often pegged to USD, which simplifies some FX considerations (less volatility), but the accounting treatment remains as per IFRS: record at historical rate and no retranslation for local books. For international companies in volatile FX environments, managing multi-currency is more complex – some may use hedge strategies to lock in costs, but that’s risk management beyond accounting entries.

Foreign Subsidiary Example: Suppose a manufacturing subsidiary in the Gulf region (say in Oman, using OMR as functional currency) purchases a production line from Germany for €1 million. The Omani company will record that asset in OMR using the rate on purchase date. Let’s say at that date €1 = 0.4 OMR, so it records the asset at 400,000 OMR. It pays the supplier six months later, during which the euro weakened to 0.38 OMR. The accounts payable initially recorded at 400k OMR is now equivalent to 380k OMR at payment, so the payable is reduced by 20k and an exchange gain of 20k OMR is recognized (the equipment effectively cost less in OMR than originally booked). The equipment stays at 400k OMR on books (non-monetary, unchanged by rate movement). Now, if this Omani subsidiary reports locally, it shows the equipment at 400k cost, depreciating maybe 40k OMR/year over 10 years. If the group in the UK consolidates it, and at year-end OMR/GBP moved, the equipment’s value will be translated at the closing rate for group statements, and that difference goes to CTA equity. Thus, each stakeholder sees the asset in their own relevant currency: local management sees it in OMR, group sees it in GBP, and neither sees wild swings in P&L from FX after acquisition.

Summary of IAS 21 Rules for Assets:

- Use spot rate on transaction date to record asset cost in functional currency[8].

- Do not update non-monetary asset carrying amounts for subsequent FX changes (if at historical cost)[8].

- Depreciate based on functional currency cost (historical rate).

- Monetary liabilities (or monetary assets) related to the purchase do get revalued at closing rates until settlement, with FX differences to P&L[8][8].

- If asset is carried at fair value, translate at rate of valuation date[8].

- In consolidation, translate foreign asset values at closing rate and send differences to OCI (CTA)[8][8].

- Disclose significant FX impacts and ensure exchange rates used are consistently applied.

This disciplined approach avoids forex transaction risk on non-monetary items and segregates translation risk to equity[11][11]. By doing so, companies present “FX-neutral” operating results – the core depreciation and asset expenses are recorded in stable functional currency terms, while pure currency fluctuations show up either in FX gains/losses (for payables, etc.) or in translation adjustments. This provides clarity to management and investors, isolating operational performance from currency noise[11].

Multi-Currency Support in ERP Systems: All major ERP systems support multi-currency accounting. Typically, an ERP will have a base currency for each company or ledger, and allow transactions in alternative currencies with conversion. For example, in ERPNext, you can set an asset’s purchase invoice in a foreign currency and specify the exchange rate or let the system fetch it[9][9]. The system will post ledger entries in base currency (and often store the foreign currency amount in parallel fields for reference). Many systems also enable parallel currencies in the General Ledger – e.g., SAP S/4HANA’s new Financial Accounting can carry transactions in up to 3 currencies (local, group, and possibly transaction currency) simultaneously, posting asset values in each. Oracle and Dynamics allow setting up secondary ledgers or reporting currencies to automatically mirror transactions in another currency[12]. This is useful for multi-national groups that want real-time reporting in a common currency.

ERP asset modules also handle that depreciation runs and postings can occur in multiple currencies/books. For instance, SAP Asset Accounting (FI-AA) has depreciation areas which can be configured for different currencies (parallel currencies) – so one depreciation area could represent local currency accounting and another could calculate depreciation in group currency, ensuring that foreign subsidiaries’ asset values are available in both their local and the group’s currency for consolidation[13][14]. Oracle E-Business Suite had a feature called Multiple Reporting Currencies (MRC) to maintain subledger data in multiple currencies, and in Oracle Cloud, one would use Secondary Ledgers in another currency for IFRS/management reporting[15]. NetSuite OneWorld supports multi-currency subsidiaries, automatically converting transactions to parent currency for consolidation[16][17].

In summary, multi-currency asset accounting requires careful adherence to standards to avoid spurious profit impacts from exchange rates. IFRS provides a clear framework: fixed assets are valued at historical rates (unless revalued) and exchange differences are handled through proper channels (P&L for monetary items, OCI for consolidation translations)[8][8]. Enterprise systems, when configured correctly, enforce these rules – ensuring that even in a multi-currency environment, a company’s asset values and depreciation expenses are recorded and reported consistently and transparently.

Enterprise ERP Systems – Fixed Assets Handling (Comparative Review)

Modern Enterprise Resource Planning (ERP) systems include dedicated Fixed Asset Management modules that automate and streamline the lifecycle of assets – from acquisition to depreciation to disposal – integrating these processes with the general ledger and other modules (purchasing, maintenance, etc.). Here we compare how several popular ERP systems (ranging from those suited to small businesses to those for large enterprises) handle fixed asset accounting, depreciation, multi-currency, and related features. We will look at ERPNext, NetSuite, SAP, Oracle ERP, and briefly Microsoft Dynamics 365, outlining each system’s capabilities, strengths, limitations, and typical use cases (small vs. large company scenarios).

ERPNext (Frappe)

ERPNext is an open-source ERP popular with small and mid-sized organizations (including many in emerging markets). It offers a full Assets module as part of its core accounting application. Features and Capabilities:

- Asset Record & Lifecycle: ERPNext maintains an Asset master record for each fixed asset, which serves as the central place to track all transactions and information related to that asset[1]. When an asset is created, you input its details (item code, purchase date, cost, location, etc.). All subsequent events – purchase (link to Purchase Invoice/Receipt), depreciation schedules, transfers (location or custodian changes), maintenance logs, asset value adjustments (write-up/write-down), and eventually selling or scrapping – are recorded against this asset record[1]. This provides a 360° view of the asset’s history. ERPNext supports marking items as fixed assets and even auto-creating asset records when purchasing such items (if configured)[1][1]. For example, if you buy 5 laptops and flag them as assets, it can auto-generate 5 asset records upon receiving the Purchase Receipt, each with its own tag and serial if needed[1][1]. This is very useful for ensuring assets are recorded promptly and accurately.

- Depreciation Management: ERPNext provides robust depreciation automation. It supports multiple depreciation methods out-of-the-box – by default Straight Line and Written Down Value (which is basically declining balance) and Double Declining Balance, plus a Manual option for custom entries[18]. You define an asset’s expected life, salvage value, and choose the method; the system then generates a depreciation schedule. You can configure depreciation frequency (monthly, quarterly, annually)[18]. At each interval, ERPNext can automatically post the depreciation journal entry to the ledger (crediting the accum. depreciation account and debiting the depreciation expense account configured for that asset’s category)[18][18]. The automation ensures you don’t miss depreciation runs. ERPNext also supports partial depreciation (if an asset is acquired mid-period or first depreciation needs proration) and will stop depreciating once an asset is fully depreciated or reaches salvage. A nice feature is Finance Books: ERPNext allows multiple depreciation books for different purposes (e.g., one book for accounting/IFRS, another for tax or managerial depreciation)[18][18]. You can record depreciation differently in each book, accommodating scenarios where tax rules diverge from accounting.

- Asset Categories and Configuration: You define Asset Categories which template key settings for assets: e.g., “Vehicles” could have a 5-year straight-line depreciation, “Computers” maybe 3-year double-declining, etc. Categories also assign the linked accounts (asset account, depreciation expense account, accumulated depreciation account, gain/loss on disposal account) so that when you create an asset under that category, those accounts auto-fill. This enforces consistency and simplifies setup.

- Asset Value Adjustments: ERPNext supports posting appreciation or impairment (write-down) through “Asset Value Adjustment” documents[18][18]. For instance, if you revalue an asset upward, you can record an increase; the system will credit a revaluation equity account and adjust the asset’s value. For impairment, it will debit an impairment expense account and reduce the asset. These adjustments integrate with accounting so the books remain balanced. However, ERPNext’s UI might not automate the nuanced IFRS logic of split between OCI and P&L for revaluation – typically one would manually decide the accounting treatment.

- Transfers and Maintenance: The module tracks Asset Movements (e.g., transfer from one warehouse or department to another)[18][18] and can log maintenance activities through Maintenance Log, linking costs or just notes about repairs. This helps in operational tracking, though it’s not as elaborate as a full Enterprise Asset Management system. It’s sufficient for most SMBs to note when an asset was serviced or relocated.

- Asset Disposal (Selling/Scrapping): ERPNext provides flows for Selling an Asset and Scrapping an Asset[18][18]. In an asset sale, you can create a Sales Invoice or Journal Entry and tag the asset, and ERPNext will compute the gain or loss on disposal, auto-posting the required entries (remove cost, remove accum. depreciation, record proceeds, book gain/loss to the configured account)[19]. For scrapping (disposal with no proceeds or junk value), it will simply write off the remaining value to a loss account. According to the docs: “‘Gain/Loss Account on Asset Disposal’ will be credited/debited based on gain/loss amount. The Gain/Loss account can be set in Company record.”[19]. This shows ERPNext simplifies the accounting at disposal time.

- Reporting: ERPNext can produce asset registers, depreciation schedules, and other reports. There are built-in Asset Reports like Asset Register (listing all assets with cost, depreciation, current value), Depreciation Ledger, and perhaps maintenance due reports[18][18]. Because ERPNext ties assets to ledger entries, you can also easily generate accounting reports (trial balance of asset accounts, etc.). The system ensures an audit trail: each asset has links to its purchase invoice, depreciation entries, and disposal entries.

- Multi-currency and Multi-company: ERPNext supports multi-currency transactions – you can record asset purchases in a foreign currency invoice, and the system will convert to your base currency for accounting[9][9]. However, one limitation historically observed (as per user forum) is that depreciation entries involving foreign currency assets require the user to mark the entry as multi-currency if the asset’s account currency differs from company currency[10][10]. ERPNext has improved multi-currency handling over time, and as of recent versions, it even integrates a currency exchange service for up-to-date rates[9]. For multi-entity setups, ERPNext can handle multi-company accounting with inter-company transactions, and each company can have its base currency. It’s possible, for example, to have a UAE company using AED and a US company using USD in one ERPNext instance; the assets would be managed per company with their respective currencies.

Strengths of ERPNext: It’s user-friendly and integrated – great for small to medium businesses that want a full asset ledger without needing an army of consultants. Setting up an asset is straightforward, and automation of depreciation is a big plus (reduces manual journal work)[18]. The fact that it’s open-source and relatively cost-effective is a bonus for cost-sensitive organizations. It covers the full lifecycle (purchase to disposal) within one system, linking with purchasing and accounting, which ensures completeness of data[4][4]. ERPNext also offers flexibility (custom fields, etc.) if a company needs to track additional asset info (like insurance, serial numbers, etc.). For companies in manufacturing or those with significant assets, having maintenance logs and movement tracking integrated is valuable.

Limitations of ERPNext: Being aimed at SMBs, it may lack some advanced features that large enterprises need. For example, component depreciation (depreciating parts of one asset separately) isn’t clearly delineated, though one could manually create multiple assets. Support for multiple depreciation books exists (Finance Books) but might not be as battle-tested or rich as in SAP/Oracle – it’s a relatively newer addition for IFRS vs Tax accounting[18]. ERPNext might not handle extremely complex scenarios out-of-the-box, such as partial disposals with proportional allocation of cost and depreciation (though the Asset Split feature covers splitting an asset)[3][3]. Also, multi-currency depreciation could be tricky if, say, an asset’s account is denominated in a different currency – one forum post described errors in posting depreciation until the multi-currency flag was checked[10][10]. These are things a large ERP might handle more seamlessly with parallel currencies. Another limitation is scalability: ERPNext can handle tens of thousands of assets, but a very large enterprise with millions of assets or extremely high transactions might require more tuning or a bigger system. However, for its target market, ERPNext covers 80-90% of needs admirably, with continuous improvements from its open-source community.

Typical Use Cases: ERPNext is well-suited for small and mid-sized companies across various industries. For instance, a manufacturing company in the Arab Gulf region could use ERPNext to manage its machinery and vehicle assets. One Oman-based manufacturing firm reported improved efficiency by using ERPNext for its asset and manufacturing management[4]. The system would allow them to track assets from procurement to disposal within one platform, handle multi-currency purchases of equipment (common in Gulf where machinery might be imported), and comply with IFRS depreciation and local reporting. SMBs that cannot afford expensive ERP licenses find ERPNext a game-changer – it brings discipline of fixed asset accounting (no more spreadsheets) with minimal cost. In summary, ERPNext’s fixed asset module offers comprehensive lifecycle management with automation at a fraction of the complexity and cost of enterprise systems, making it ideal for growing businesses and even larger entities in developing markets that value flexibility and open-source.

Oracle NetSuite (Fixed Assets Management SuiteApp)

NetSuite is a cloud-based ERP popular among mid-market companies and rapidly growing firms (including many tech startups, SaaS companies, etc., and increasingly larger enterprises). Its core finance module originally did not include fixed asset accounting out-of-the-box, but Oracle NetSuite offers a Fixed Asset Management (FAM) SuiteApp that can be installed to provide a full asset module. Let’s discuss NetSuite’s fixed asset handling:

- Asset Management SuiteApp: NetSuite’s FAM module, once enabled, integrates with purchasing, accounts payable, and the general ledger. It automates the complete asset lifecycle from acquisition to disposal[5], aiming to eliminate the need for external spreadsheets. A key benefit noted is that it supports managing assets across multiple entities, currencies, and accounting standards centrally[5][5]. The SuiteApp provides a dashboard and forms for creating and tracking assets.

- Asset Creation: Assets in NetSuite can be created automatically from transactions or manually. For example, when you enter a Vendor Bill (supplier invoice) for a capitalizable item (like purchasing machinery), FAM can be configured to automatically generate a new asset record from that bill[5]. This uses item categories or account mapping: if an expense hits a fixed asset account, trigger asset creation. Alternatively, you can manually create an asset and link it to a purchase transaction or journal. This automation ensures no asset slips through without being recorded – a significant internal control advantage. NetSuite also supports asset creation via multiple sources: purchase orders, vendor bills, journal entries (e.g., if capitalizing a constructed asset via a journal)[5].

- Depreciation Automation: NetSuite FAM allows defining Depreciation Methods (straight line, declining balance, sum-of-years, units of production, etc.) and useful lives. It will then automatically calculate depreciation each period and post depreciation journals to the GL[5]. You can set conventions (like full-month or half-month conventions), depreciation start dates, and so on. The module can generate schedules and you can either have it post monthly automatically or on-demand. Importantly, NetSuite supports multiple depreciation books (“Multi-Book Accounting”) – which is one of its strengths for companies reporting under multiple frameworks (e.g., GAAP and IFRS, or book vs tax). With multi-book, an asset can have parallel depreciation schedules in, say, a Corporate Book and a Tax Book. NetSuite will keep track of both and allow reporting in either basis. This means a company can manage both IFRS depreciation and local tax depreciation simultaneously, which is crucial for compliance. The FAM SuiteApp fully integrates with NetSuite’s multi-book feature[5].

- Asset Classes and Templates: The FAM module provides for Asset Categories/Types where you define default depreciation methods, life, and accounts (similar to other ERPs)[5][5]. For instance, “Office Equipment” category might default to 5-year straight-line, etc. This standardizes data entry and reduces errors.

- Transactions – Transfers, Revaluations, and Disposals: NetSuite supports asset transfers between departments or subsidiaries (if within the same OneWorld environment). If transferring between subsidiaries (different legal entities), it can either treat it as an intercompany sale or transfer with net book value – depending on configuration. Revaluation or write-up/down can be done via an “Asset Revaluation” transaction in the SuiteApp, which allows you to increase or decrease an asset’s value and specify the accounting (gain to revaluation reserve or loss to expense). The module will then adjust future depreciation accordingly[5]. Impairments would be handled as a partial write-down similarly. NetSuite also handles asset splits and merges if needed (e.g., splitting one asset into two, or combining multiple low-value assets into a single asset for simplicity). For retirements/disposals, the module can process a sale or discard: you input the sales proceeds (if any) and it calculates the gain or loss and generates the GL entries to write off the asset and record the gain/loss[5][5]. It can even handle partial disposals (disposing some quantity of an asset, say you initially capitalized 10 identical items as one asset and then sell 2 of them – it can proportionately remove cost and depreciation).

- Audit Trails and Reporting: A notable feature of NetSuite FAM is auditability – each asset has an audit trail of all actions (creation, depreciation runs, changes, disposals). Standard reports include Depreciation Schedules, Asset Register, Asset Summary, etc. NetSuite’s reporting can consolidate asset data across subsidiaries if needed (great for group reporting). Also, being cloud-based, it offers real-time visibility to all asset data. The SuiteApp includes compliance features like ensuring no depreciation is missed and providing audit logs for each asset.

- Multi-Currency & Multi-Entity: NetSuite OneWorld is built for multi-subsidiary and multi-currency. Each subsidiary has a base currency, but you can transact in foreign currencies easily. For fixed assets, if a subsidiary buys an asset in another currency, the base currency value is recorded based on the rate on that date (and as discussed, that stays as historical cost). NetSuite will handle the depreciation in the subsidiary’s base currency automatically. If consolidating to a parent with different currency, NetSuite will translate the subsidiary’s results (including depreciation and asset balances) using the appropriate consolidation rate (assets at closing rate, depreciation at average rate typically – it’s compliant with GAAP/IFRS for translation). The system thus inherently supports multi-currency asset accounting and reporting. One resource highlights that NetSuite’s multi-currency feature supports 190+ currencies and can produce real-time consolidated financials in a parent currency[16][17]. In the context of fixed assets, that means a CFO can see, for example, the total net book value of all assets in USD across a multinational company, even if local books are in EUR, GBP, etc., with NetSuite handling currency conversion in the background.

- Multi-Book (Multiple Accounting Bases): This is a big advantage for companies in jurisdictions that have to report under two standards. NetSuite FAM with multi-book will let you maintain an IFRS depreciation schedule and, say, a local GAAP or tax schedule for the same asset concurrently[5]. You can then produce financial statements or depreciation reports under either basis at the click of a button. This is extremely helpful for companies operating in places like the Middle East where they might need IFRS for group and maybe local regulations for statutory/tax, or for US-based multinationals needing GAAP vs tax.

Strengths of NetSuite: It’s a cloud solution, so updates (like new depreciation rules or currencies) are automatically available. The Fixed Asset module is quite comprehensive after years of improvement – covering lifecycle fully: “automates depreciation, manages asset transfers and disposals, and ensures compliance; all within one system, eliminating spreadsheets”[5]. NetSuite’s strength is in integration: fixed asset accounting is tied to purchasing (so assets are captured when bought), tied to the GL (depreciation and disposal entries seamless), and tied to financial reporting (multi-book, consolidation). NetSuite is also relatively user-friendly with a modern interface and good dashboards for asset managers. For mid-size firms, it offers enterprise-grade capabilities (multi-currency, multi-entity, audit trails, role-based access) without the heavy IT overhead of something like SAP. Also, being highly configurable, businesses can tailor depreciation methods, conventions, and asset categorization to their needs easily from the UI.

Limitations of NetSuite: The FAM module is an add-on SuiteApp – in some cases it might cost extra or require enabling (though Oracle often bundles it now for larger editions). Early versions of FAM had some quirks and performance issues with large volumes, but these have improved. Still, if a company has hundreds of thousands of assets, they’d want to ensure NetSuite can handle the depreciation runs efficiently (which it generally can, but may not match the sheer industrial strength of SAP which is designed for millions of assets and deep customization). Another limitation might be in extremely complex scenarios – e.g., if you need to depreciate one asset differently in 4 or 5 different books (NetSuite multi-book usually covers up to 3 or so statutory books per subsidiary). Also, NetSuite being multi-tenant cloud, some customization (like very custom asset reporting or complex integrations) might be less flexible than an on-prem system. However, these are minor for most use cases.

Typical Use Cases: NetSuite is often used by mid-market companies and divisions of enterprises. For example, a regional manufacturing company or a global e-commerce firm might choose NetSuite OneWorld to manage finances across subsidiaries. If such a company has, say, a manufacturing plant in one country (with heavy machinery) and offices in others (with IT equipment and vehicles), NetSuite can manage all those assets in one place. Case Study: A good illustrative case is a company like Paysend, a fintech that used NetSuite OneWorld to centralize financial data for multi-country operations[20]. While not manufacturing, it highlights multi-currency – but a manufacturing example could be a company that has production equipment in multiple countries: NetSuite would allow tracking each asset in its local subsidiary, depreciating per local rules, and then consolidating. Another scenario: a multi-location healthcare provider implemented ERPNext (similar SMB context) for multi-currency and multi-company asset management[21]. For NetSuite specifically, many tech companies going global adopt it – they might not have huge PPE, but those that do (like companies that own data center equipment globally) find FAM useful to keep track of servers, etc. Strength in multi-subsidiary support means if a company grows by adding foreign entities, NetSuite scales with them, whereas something like ERPNext might require more manual setup.

In summary, NetSuite’s Fixed Asset Management provides a robust, automated solution for asset lifecycle with the cloud advantage. It brings enterprise-level features (multi-book, multi-currency, multi-entity, audit controls) in a package accessible to mid-sized firms. It’s ideal for companies outgrowing basic accounting software and spreadsheets, who need stronger internal controls and multi-entity consolidation.

SAP (Financial Asset Accounting – FI-AA)

SAP (particularly SAP ERP ECC and S/4HANA) is known for its deep and comprehensive Financial Accounting modules. SAP’s Asset Accounting (FI-AA) is a sub-ledger integrated with SAP’s Finance module and is widely used by large enterprises and complex organizations (manufacturing, utilities, etc.). It is very feature-rich and highly configurable to meet various accounting requirements around the world. Key aspects of SAP’s fixed asset handling:

- Integration and Master Data: SAP’s asset management is tightly integrated with other modules: you typically purchase assets via the MM (materials management) module, linking to FI-AA so that when a capital goods PO is received, an asset under construction or final asset can be created. The heart is the Asset Master Record – similar concept to others, it stores details of each asset: asset class, description, location, cost center allocation (for depreciation expense tracking by department), etc.[22][22]. Assets are organized by Asset Class which governs their default depreciation rules and GL accounts. For example, Asset Class 1000 – “Plant Machinery” might be linked to GL account for Plant & Equipment, a depreciation key for 10-year straight-line, etc. You can have thousands of asset masters; SAP is designed to handle large volumes (organizations with 100k+ assets). The asset master also allows component structure (main asset with sub-numbers for components).

- Asset Lifecycle in SAP: SAP FI-AA provides functionality for the entire lifecycle[22][22]. Highlights:

- Acquisition: Assets can be acquired through external purchase (PO/vendor invoice), internal production (capital projects – integrated with Investment Management/Projects System), or direct FI journal. When posting an acquisition, SAP records the value in the asset sub-ledger and automatically posts to the appropriate Asset GL and offset (AP or bank)[22]. There is support for acquisition on specific dates, and it can calculate depreciation start accordingly (SAP by default uses value date for start of depreciation, with options for half-month conventions etc. as config).

- Depreciation Calculation & Posting: SAP automatically calculates depreciation via configured Depreciation Keys which can embody straight-line, declining balance, multi-level rates, etc. (SAP’s depreciation key configuration is extremely flexible – e.g., you can set a declining balance switch to straight-line when it yields higher expense, etc.). Depreciation is generally run as a batch job periodically (often monthly). The Depreciation Run program will calculate depreciation for all assets and post one aggregated entry per depreciation area (or asset if needed) to the GL[23]. It updates the Asset values and posts to expense and accum. depreciation accounts. SAP ensures these postings are consistent with accounting principles and allows various conventions[22][22]. The depreciation is tracked in depreciation areas which represent different bases (more on that soon). SAP also handles special depreciation (like bonus depreciation or accelerated rates for tax) and unplanned depreciation (impairment) through separate transactions.

- Mid-life Adjustments: If an asset’s useful life needs change, or its value needs to be increased (subsequent acquisition) or partially retired, SAP has transactions for adjustments[22][22]. For example, you can post an “unplanned depreciation” to write it down (impairment), which immediately hits the asset value and records an expense. Or you can change the useful life in the asset master and SAP will prospectively recalc remaining depreciation (accounted for as change in estimate under IAS 8). Revaluations under IFRS can be handled via an Revaluation program (moving asset to fair value and adjusting equity); historically many SAP users in IFRS contexts used a separate depreciation area to handle the revaluation increment.

- Transfers: SAP allows transferring an asset’s value to another asset or between company codes. For internal transfers (like moving an asset from one cost center to another or one asset class to another within same company), you can do an asset transfer posting which reassigns the remaining value. If moving across company codes (entities), it can do an intercompany asset transfer by retiring it from one and acquiring in another, possibly recognizing a intercompany sale.

- Retirement/Disposal: When disposing of an asset (sale or scrap), SAP’s transaction will remove the asset’s cost and accumulated depreciation, ask for sale proceeds if any, and compute the gain or loss[22][22]. It posts the necessary entries (debit cash, debit accum dep, credit asset cost, credit gain or debit loss). SAP even has functionality to handle partial retirement (retiring a portion of asset value, say you dismantle part of a composite asset). You can retire by quantity or percentage, and SAP will proportionally remove cost and depreciation. This is handy for assets capitalized as a group.

- Reporting: SAP provides a wealth of standard reports: Asset Explorer (drill-down on one asset’s transactions and depreciation schedule), Asset History Sheet (a comprehensive report showing beginning balance, acquisitions, disposals, depreciation, ending balance for each asset or class)[22][22], depreciation comparison reports, etc. The Asset History Sheet is often used for financial statement disclosures, and SAP can configure it to match local reporting formats. SAP also can produce tax reports if separate depreciation areas for tax are maintained. Because SAP stores each depreciation area’s values, reporting under different bases is straightforward. Additionally, SAP has tools for physical inventory integration (tracking if assets have been verified on site) and can integrate with barcode/RFID for asset tracking[22].

- Parallel Accounting & Multi-Currency: One of SAP’s strongest features is handling parallel accounting via Depreciation Areas. A depreciation area in SAP represents a set of accounting rules (e.g., book accounting, tax accounting, IFRS accounting, local GAAP accounting). For example, Depreciation Area 01 might be local GAAP (posting to leading ledger), Area 30 might be IFRS (posting to non-leading ledger or just for reporting), Area 15 might be Tax (not posting to GL, just tracking values). You can configure depreciation keys differently per area if needed. This allows a single asset master to have multiple valuation bases. For instance, an asset could have 10-year life in Area 01, but maybe accelerated 5-year in Area 15 for tax. SAP will maintain two sets of values and depreciation schedules. This ensures compliance with multi-GAAP requirements – something essential for large firms operating under e.g., local GAAP vs IFRS concurrently[24][25]. With S/4HANA, SAP improved this via Universal Journal that can hold multiple valuations and ledger group postings.

- In terms of multi-currency, SAP can manage up to 3 currencies for each asset posting (for example: local currency, group currency, and maybe transaction currency). If parallel currencies are set in the GL, when you post an asset acquisition, SAP will record values in all configured currencies (using exchange rates from its rate tables). Depreciation then is calculated in each currency as well. SAP ensures that the depreciation in group currency, for instance, is based on the asset’s group currency historical cost, and it will follow the same pattern (thus it doesn’t introduce exchange gains/losses each period, it’s essentially doing what IFRS says: use historical rate for non-monetary in that currency and depreciate that)[13][14]. If you use group currency depreciation area, at consolidation you have readily available the depreciation and asset balances in group currency, which simplifies consolidation adjustments (no need to recompute fixed asset translations, though under IFRS you’d typically still translate at closing rate for consolidation – however, SAP’s approach means your group currency ledger will show translation differences in equity automatically). All in all, SAP’s multi-currency handling is very advanced – appropriate since many large SAP customers are multinationals. It even has features like index-based revaluation for inflation accounting or currency devaluation scenarios (IAS 29 hyperinflation accounting).

- Advanced Features: SAP FI-AA shines with advanced capabilities often needed by large enterprises:

- Component Accounting: You can split an asset into components (sub-assets) with different depreciation (e.g., an aircraft can have engines as separate depreciable parts). IFRS requires component depreciation for significant parts[2], and SAP supports this by allowing multiple asset master records linked or using asset sub-numbers.

- Asset Under Construction (AuC): SAP has robust support for assets in progress. Companies often accumulate costs (via Investment Orders or WBS projects) which settle into an AuC asset. When the asset is ready, a simple transfer places the value into a completed asset, and depreciation begins. This keeps construction costs separate from depreciable assets until ready (following IAS 16’s rule that depreciation begins when asset is available for use).

- Leased Assets: With the new leasing standards (IFRS 16/ASC 842), SAP provides solutions (either via its Real Estate module or Lease Accounting engine) to handle right-of-use assets. But even in core FI-AA, one could manage finance lease assets historically. There are also features to handle asset retirement obligations (like decommissioning costs) by capitalizing and amortizing those (some use SAP provisions).

- Mass Processing: SAP can process large volumes in batch – mass changes of useful life, mass transfers, or mass disposals. This is crucial for companies with many assets.

- Physical inventory integration: As noted, SAP can integrate with barcode/RFID systems to reconcile physical asset counts with the books[22].

- Extensibility: You can attach documents to asset master (like pictures, manuals), maintain custom fields (e.g., serial number, responsible person), and integrate with maintenance modules (like SAP PM – Plant Maintenance – to link maintenance orders to assets).

- Strict Control: SAP ensures that financial postings and asset sub-ledger are always reconciled. In SAP, the asset subledger is always in sync with GL because transactions simultaneously update both (no manual GL entries allowed that would diverge).

Strengths of SAP: Simply put, breadth and depth. SAP FI-AA has been developed and refined over decades and can handle virtually any scenario: complex tax depreciation laws (via depreciation keys), multi-GAAP, multi-currency, huge volumes, detailed reporting, etc. It is highly compliant – used by companies globally, it supports IFRS, US GAAP, and many local requirements via configuration (for example, you can set up half-year conventions for US, inflationary adjustments for certain countries, etc.). For large enterprises especially, SAP provides the scalability and controls needed: you can trust that every asset transaction hits the books correctly. Also, integration with SAP’s ecosystem (MM, PM, CO) means assets are not an isolated module; they fit into the whole enterprise process flow (procurement to fixed asset to depreciation to cost accounting, etc.). Another plus is auditability – SAP logs changes, and the Asset History reports provide clear movement schedules that auditors love[22].

SAP’s multi-currency and parallel ledger capability is particularly beneficial for say, a multinational manufacturing company that has to produce both local statutory statements and a consolidated IFRS report – SAP can produce both from one system with minimal manual adjustments[22][22]. Many Fortune 500 industrial and oil & gas companies rely on SAP for precisely these reasons – e.g., Saudi Aramco’s joint ventures like SASREF implemented SAP to handle their operations and finance, benefiting from integrated product costing and asset management[26][26].

Limitations of SAP: The flip side of SAP’s power is complexity and cost. Implementing SAP FI-AA requires knowledgeable consultants to configure asset classes, depreciation keys, areas, etc. It’s not as out-of-the-box for a small company – typically, a smaller firm wouldn’t use SAP at all given the investment needed. SAP’s user interface historically was more transactional (though Fiori apps in S/4 have improved usability), meaning it’s not as intuitive to a new user as, say, ERPNext or NetSuite. Also, flexibility comes with constraints – e.g., once an asset is capitalized, changing its class or depreciation area requires careful posting or sometimes isn’t allowed without resetting data. Companies must also carefully plan data migration to SAP if coming from another system (to populate the accumulative values correctly).

For very unique requirements, sometimes SAP’s standard functionality may require custom development. For instance, IFRS requires componentization – SAP handles that by multiple assets; some might want a more hierarchical view. But usually SAP can be bent to the task. Another potential limitation: cost – licensing SAP for asset management is part of core FI, but the bigger cost is implementation and maintenance. Also, if a company only wants a fixed asset solution and not a full ERP, SAP isn’t modular in that sense (though SAP has Business One for smaller cos, and one could theoretically just use FI/AA, but typically you get the whole suite).

Typical Use Cases: SAP is typically seen in large enterprises, multi-nationals, and asset-intensive industries. For example, a large manufacturing conglomerate in the Gulf might use SAP to manage its assets across various plants. They might have thousands of assets (machines, vehicles, buildings) across subsidiaries in different countries. SAP would allow them to maintain each subsidiary’s ledger in local currency, depreciate per local rules, and also maintain an IFRS ledger. The system can handle special regional needs (like in some Gulf countries, WDV method is popular for tax). Case Study Example: Consider a Middle Eastern oil & gas company – they have extremely high-value assets (refinery units, pipelines) with complex accounting (some are joint ventures). SAP is frequently the go-to ERP in oil & gas; it can manage their massive asset base and integrate with maintenance. In fact, companies like Saudi Aramco and its JV’s have used SAP to achieve better visibility and control over assets, as SAP’s own materials indicate improved asset utilization and shutdown control through better data[26][26]. Another example is a global automotive manufacturer – they operate in dozens of countries, each with different depreciation rates and currencies. SAP’s parallel ledger and depreciation areas make it possible for one unified system to produce local books and one global book, a huge efficiency in global consolidation.

In summary, SAP Asset Accounting is the gold standard for comprehensive fixed asset management in large-scale, complex environments. It offers unparalleled functionality and compliance capabilities, at the cost of higher complexity. For a large enterprise requiring precision and integration (e.g., manufacturing, oil & gas, utilities, transportation), SAP is often chosen because it can model their asset accounting with all the nuance required – from tracking every last bolt in a plant to consolidating multi-currency financials. It is often considered overkill for small companies, but for big ones, its strengths align perfectly with their needs.

Oracle ERP (Oracle E-Business Suite & Oracle Cloud ERP)

Oracle’s ERP solutions also provide robust fixed asset management. Historically, Oracle E-Business Suite (EBS) had a module called Oracle Assets, and more recently Oracle Cloud ERP has a Fixed Assets module. We’ll outline their general capabilities (they are similar in philosophy to SAP’s, with some differences).

- Oracle Assets (E-Business Suite): In Oracle EBS, Fixed Assets is part of the Oracle Financials suite. It covers four main processes: Additions, Adjustments, Depreciation, and Retirements[27][27]. This aligns with the lifecycle we discussed. Oracle Assets provides asset tracking integrated with Oracle Payables (you can create assets from AP invoices), and Oracle Projects (to capture construction in progress). Key features:

- Additions: You add assets either manually or from AP invoices. Oracle Assets had a concept of Asset Books – e.g., a corporate book, a tax book. You would add an asset to a book (or link books for same asset with different conventions). When adding, you specify category, cost, date, depreciation method, etc.

- Depreciation: Oracle calculates depreciation through a depreciation engine. You run depreciation periodically. The formulae and methods available are similar (straight line, DDB, SYD, units, etc.). Oracle can handle prorated conventions (like mid-month, following month, etc.). Depreciation can be run for each asset book, and Oracle Assets will not let you close a period until depreciation is run (ensuring no pending depreciation).

- Adjustments: If you need to adjust asset cost (add cost, or credit some cost), Oracle handles it as an “Adjustment” transaction. Changing useful life or method is also an adjustment. These can trigger catch-up depreciation or prospectively change future depreciation.